Key Takeaways

- Hail damage repairs range from $150 to $7,500 for targeted fixes; full commercial roof replacements can exceed $25,000 depending on roof size and system type

- Membrane type, total affected square footage, and structural layer damage drive the widest cost swings on commercial roofs

- Minor damage (a few shingles, localized bruising) typically costs under $1,000; widespread structural damage can reach $12,500+

- Standard commercial insurance policies cover hail damage; filing within 48 hours and getting a contractor on-site quickly limits further exposure and strengthens your claim

How Much Does Hail Damage Roof Repair Cost in 2026?

Hail damage repair costs vary widely based on damage severity, roof type, material, and location. Delaying a professional inspection is the most common budgeting mistake — secondary damage that develops in the weeks after a storm can turn a straightforward repair into a partial or full replacement.

Minor Repairs

Localized damage—replacing a handful of shingles, patching cracked flashing, or sealing bruised areas—typically costs $150 to $1,400. This tier covers surface-level fixes where structural components remain intact, usually requiring 2-4 hours of labor and minimal materials.

Minor repairs don't account for:

- Hidden underlayment damage beneath intact surface materials

- Decking compromise from moisture intrusion

- Granule loss patterns spanning multiple slopes

Moderate Repairs

Multi-area damage requiring partial re-roofing, decking repair, or vent replacement runs $1,400 to $7,500. Jobs reach this tier when:

- Granule loss affects multiple roof slopes

- Underlayment shows water staining or saturation

- Flashing systems require full replacement

Moderate repairs typically involve removing and replacing 30-50% of the roof surface, plus secondary damage that isn't visible from the ground.

Major Repairs and Full Replacement

Widespread or structural hail damage drives costs to $7,500 to $25,000+ depending on square footage and material. A "repair" becomes a "replacement" when damage covers more than 50% of the roof surface, the structure is nearing end of life, or repair estimates approach half the cost of full replacement.

For commercial properties, major replacements on facilities exceeding 10,000 square feet can exceed $50,000.

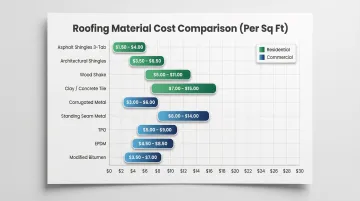

Material Cost Comparison Table

| Material | Installed Cost per Sq. Ft. |

|---|---|

| Asphalt Shingles (3-tab) | $3.00 – $6.00 |

| Asphalt Shingles (Architectural) | $4.00 – $9.00 |

| Metal (Corrugated) | $7.00 – $12.00 |

| Metal (Standing Seam) | $8.00 – $22.00 |

| Clay/Concrete Tile | $10.00 – $25.00 |

| Wood Shake/Shingles | $4.50 – $15.00 |

| TPO (Commercial Flat) | $4.00 – $14.00 |

| EPDM (Commercial Flat) | $4.25 – $13.00 |

| Modified Bitumen (Commercial Flat) | $4.00 – $8.00 |

Key Factors That Affect Hail Damage Repair Costs

Pricing is shaped by a combination of physical, material, and operational variables. Understanding each helps building and facility owners budget accurately and negotiate with contractors from a position of knowledge.

Roof Material

Material type is the biggest single cost driver. Commercial flat roof systems span a wide range depending on membrane type and installation method:

- TPO and EPDM membranes: $4–$14/sq ft

- Modified bitumen systems: $4–$8/sq ft

- Standing seam metal: $15–$22/sq ft or more

- Asphalt shingles (low-slope or hybrid applications): $4–$9/sq ft

Premium materials like standing seam metal cost roughly double upfront, but deliver 40–70 year lifespans and can qualify for insurance premium discounts of 5–35%.

Extent and Location of Damage

Damage location matters as much as size. Flashing, decking, skylights, and roof vents are more expensive to repair than surface membranes—flashing repairs alone average $200 to $600, but can reach $1,000 for complex installations. Hail-induced granule loss on asphalt is often invisible from the ground but dramatically shortens roof lifespan if left unaddressed. Damage concentrated near roof penetrations or valleys requires more labor and precision than open-field shingle replacement.

Roof Size and Pitch

Larger roofs require more material and more labor hours, driving up costs proportionally:

- 1,000 sq ft: $3,750 – $11,000

- 1,500 sq ft: $5,625 – $16,500

- 2,000 sq ft: $7,500 – $22,000

- 3,000 sq ft: $11,250 – $33,000

Steep-pitched roofs (7/12 or higher) add safety complexity and labor cost. OSHA safety requirements, scaffolding, and slower installation speeds incur a 20% to 50% labor premium. A pitch multiplier is used to calculate the true surface area—a 6/12 pitch has a multiplier of 1.118, while a 12/12 pitch has a multiplier of 1.414.

Labor Rates and Local Market

Roofing labor typically runs $40 to $90 per hour per worker, and even minor repairs usually require at least two workers for safety. In Southeast Texas, the mean hourly wage for roofers is $21.39 statewide, with Houston-area rates at $22.43 and Beaumont-Port Arthur at $25.72. Post-storm surge pricing can temporarily inflate costs—Verisk documented a 7.5% spike in replacement costs in DFW just weeks after a May 2024 storm. Secure contractor agreements within 48 hours of a storm to lock in baseline rates before regional demand inflates pricing.

Inspection Fees and Hidden Damage

A professional roof inspection ($150–$600) is a necessary upfront cost that often pays for itself by revealing hidden damage. Compromised underlayment, damaged decking, and weakened flashing escalate into much costlier repairs if left undetected.

Key inspection options for commercial roofs include:

- Standard inspection ($150–$600): Identifies surface damage, flashing failures, and penetration issues

- Drone-assisted inspection: 54% of roofing contractors now use drones as of 2026, making aerial assessments a standard option for larger commercial roofs.

- Thermal imaging ($400–$600): Detects hidden moisture beneath flat commercial membranes (TPO/EPDM) and can speed up claims approval

Repair vs. Replace: When Each Makes Financial Sense

Deciding between repair and replacement after hail damage is one of the most consequential (and commonly mishandled) financial decisions a property owner faces. Getting it wrong in either direction — under-repairing or prematurely replacing — has real cost consequences.

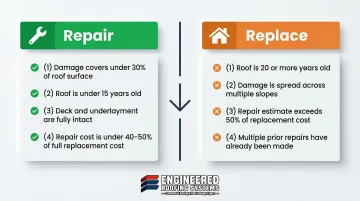

Repair is the right call when:

- Damage is localized to less than 30% of the roof surface

- The roof is under 15 years old

- The structural deck and underlayment are intact

- Repair costs fall meaningfully below replacement cost (typically under 40–50%)

Full replacement is more cost-effective when:

- The roof is nearing end of life — 20+ years for asphalt shingles, 15+ years for 3-tab; 15–20 years for single-ply membranes (TPO/PVC) on commercial properties

- Damage covers multiple slopes or the majority of the surface

- Repair estimates climb above 50% of replacement cost

- Multiple prior repairs have been made, indicating systemic failure

These thresholds hold for both residential and commercial properties, though commercial roofs introduce added variables. For industrial and commercial buildings in Southeast Texas, the right call often hinges on membrane condition, insulation integrity, and remaining system life — not just visible surface damage. Engineered Roofing Systems conducts detailed post-hail assessments for commercial and industrial properties across the Houston area, helping owners determine whether targeted repair or full replacement delivers better long-term value.

Using Insurance to Cover Hail Damage Repairs

Commercial property insurance policies almost always cover hail damage — unlike flood or earthquake coverage — but the payout you receive depends heavily on your policy terms. Deductibles, roof age limitations, ACV vs. RCV policy type, and filing deadlines all shape what you'll actually collect.

ACV vs. RCV: How Policy Type Affects Your Payout

Older roofs — typically 15–20+ years — are the most vulnerable to reduced payouts under actual cash value (ACV) policies. Insurers factor in depreciation, which can dramatically cut your claim. For example, a 15-year-old roof with a $20,000 replacement cost might carry $12,000 in depreciation under an ACV policy, leaving you responsible for $14,000 out-of-pocket after a $2,000 deductible.

Replacement cost value (RCV) policies cover the full repair or replacement cost regardless of roof age — a meaningful difference when a commercial roof replacement runs $50,000 or more.

Texas-Specific Filing Deadlines:

- Insurers must acknowledge receipt of a claim within 15 days

- Claims must be accepted or rejected within 15 business days of receiving all required information

- Payment must be made within 5 business days of notification

- Texas statute of limitations allows two years from the date of damage to file a property damage claim

- TWIA (Texas Windstorm Insurance Association) policyholders have one year from the date of damage to report a claim

Maximize your insurance claim:

- Get a professional inspection and document damage with photos before any temporary repairs

- File promptly—within 48 hours if possible

- Hire a contractor experienced with insurance claims who can coordinate directly with the adjuster

- Keep receipts for all emergency protective measures (tarps, temporary sealing)

How to Reduce Your Hail Damage Roof Repair Bill

Contact your insurance provider first and confirm your deductible before accepting any contractor quote. In most hail events, insurance covers the bulk of legitimate repair costs — your deductible is often the only true out-of-pocket expense.

Get at least three quotes from licensed, bonded, and insured contractors. Watch for storm chasers who show up immediately after a major event and push for a quick sign-off — they rarely have the manufacturer certifications that protect your warranty. When vetting contractors, look for:

- Documented experience with your specific roof type (especially critical for commercial membrane systems)

- Authorized status with major manufacturers such as Versico, Carlisle, Duro-Last, or ASTEC

- Proof of bonding and insurance before any work begins

Engineered Roofing Systems holds authorized contractor status with all four manufacturers above, meaning repairs meet manufacturer standards and qualify for extended warranties.

Act quickly: Delayed repairs allow water infiltration that breeds mold within 24-48 hours. Industry data shows delayed assessments (60+ days) escalate remediation costs by 340%—turning a $300 flashing fix into a $3,000-$12,000 structural nightmare. For commercial facilities, that cost escalation can mean the difference between a targeted repair and a full membrane replacement.

Frequently Asked Questions

How much does hail damage roof repair cost?

Typical hail damage repairs range from $150 to $7,500 for targeted fixes, with the national average around $1,160–$4,250 depending on severity. Full replacements on larger or premium-material roofs can exceed $25,000.

Will homeowners insurance cover hail damage to my roof?

Standard homeowners and most commercial property insurance policies cover hail damage as a named peril, though payout is subject to your deductible and policy type. File within the insurer's deadline—typically one to two years after the storm—to preserve your claim.

Is it worth repairing hail damage, or should I replace the roof?

Repair makes sense when damage is localized and the roof is relatively young. Replacement becomes the better call when the roof is aging, damage is widespread, or repair costs approach 50% of replacement value.

Will insurance cover a 17-year-old roof?

Coverage depends on policy type. Replacement cost value (RCV) policies cover full repair/replacement regardless of age, while actual cash value (ACV) policies depreciate older roofs and reduce the payout. Call your insurer to confirm which you have before filing.

Is $30,000 too much for a roof?

$30,000 can be within range for large commercial roofs, premium materials (slate, standing-seam metal), or roofs with extensive hail damage requiring full replacement. For any project in this range, getting at least two or three competitive quotes is always worth the time.

Is it expensive to fix roof flashing?

Flashing repair typically costs $150–$1,000 depending on the length of damaged flashing and the material. Damaged flashing is a high-priority repair because it's a primary entry point for water, meaning delays significantly increase the risk of interior water damage.